How I Cracked Financial Freedom Without Risking It All

What if financial freedom isn’t about making more, but spending less on the right things? I used to think earning big was the key—until I analyzed every dollar I spent. That shift changed everything. By focusing on cost patterns, not just income, I built a life with real flexibility. This isn’t a get-rich-quick scheme. It’s a tested, thoughtful journey from stress to stability. Let me walk you through how simple cost awareness became my most powerful financial tool. What started as curiosity about monthly bills turned into a complete transformation of my financial mindset. I stopped measuring success by income and began valuing control, clarity, and choice. And the best part? It didn’t require a promotion, a side hustle, or risky investments. It only required attention—something everyone has, regardless of salary or savings. This is the quiet, sustainable path to real financial freedom.

The Myth of More: Why Earning Bigger Isn’t the Answer

For years, the promise of a higher salary felt like the golden ticket. A raise meant breathing room, relief, maybe even freedom. But time and again, that extra income disappeared just as quickly as it arrived—funneled into a newer car, a larger apartment, or more frequent takeout. The pattern was clear: every financial gain was quietly offset by a proportional increase in spending. Economists call this lifestyle inflation, and it’s one of the most common barriers to true financial progress. The belief that more money solves money problems is deeply ingrained, but it’s also dangerously misleading. Income growth without spending discipline doesn’t lead to freedom—it leads to a more expensive version of the same stress.

Consider the typical career arc: a professional earns a promotion, gains $10,000 in annual income, and uses it to upgrade their lifestyle. The old sedan becomes a leased SUV. The modest apartment turns into a higher-rent unit closer to work. Gym memberships, streaming services, and weekend outings multiply. On paper, they’re earning more. In reality, their financial flexibility may have shrunk. Why? Because their fixed and habitual expenses now consume a larger portion of their income. They’re not wealthier—they’re more committed. This creates a fragile financial state where any disruption, such as a job loss or medical issue, can trigger crisis. The higher salary didn’t build resilience; it increased exposure.

The real issue isn’t ambition or earning potential—it’s the assumption that income alone determines financial health. In truth, control over spending is far more powerful than the size of a paycheck. A person earning $60,000 who lives on $45,000 has more freedom than someone earning $100,000 who spends $95,000. The gap between income and outflow—the surplus—is what fuels security, options, and peace of mind. That surplus doesn’t come from chasing raises. It comes from intentional choices about what to fund and what to forgo. Shifting focus from earnings to expenditures is the first step toward lasting financial stability. It’s not about deprivation. It’s about direction—aligning spending with values, not impulses.

Mapping Your Money: The First Step to Real Control

Before you can change your financial path, you need to see where you currently stand. That begins with tracking your money—not perfectly, but consistently. Many people avoid this step, fearing it will feel like financial surveillance or require complex spreadsheets. But it doesn’t have to. The goal isn’t accounting precision; it’s awareness. Even a simple three-week log of transactions can reveal surprising patterns. Use a notebook, a notes app, or a basic budgeting tool—what matters is regular recording of every expense, from rent to coffee to online subscriptions. The act of writing things down creates a mental shift. Suddenly, money isn’t an abstract number in a bank account. It’s a series of choices, each with a consequence.

Once you’ve gathered a few weeks of data, the next step is categorization. Group expenses into three broad buckets: essentials, flexibility zones, and leaks. Essentials are non-negotiable costs—housing, utilities, groceries, insurance, and minimum debt payments. These keep life functioning. Flexibility zones include spending that supports well-being but can be adjusted—dining out, entertainment, clothing, or travel. These are not wasteful, but they are negotiable. Then come the leaks—small, recurring expenses that often go unnoticed but add up over time. These include unused subscriptions, impulse purchases, convenience fees, or automatic renewals for services no longer used. Leaks are especially dangerous because they feel insignificant in the moment but compound into major outflows over months and years.

One woman discovered she was spending $180 a month on three streaming services, two of which she hadn’t opened in months. Another realized her “quick” lunch orders averaged $200 per month—more than her grocery bill for household snacks. These insights weren’t about shame. They were about clarity. When you see your spending mapped out, you stop guessing and start deciding. You can look at a $15 monthly subscription and ask: Does this add real value to my life? Is it worth the trade-off? This kind of reflection turns passive spending into active stewardship. It’s not about cutting everything. It’s about aligning outflows with priorities. And once you understand your current habits, you’re in a far stronger position to make changes that stick.

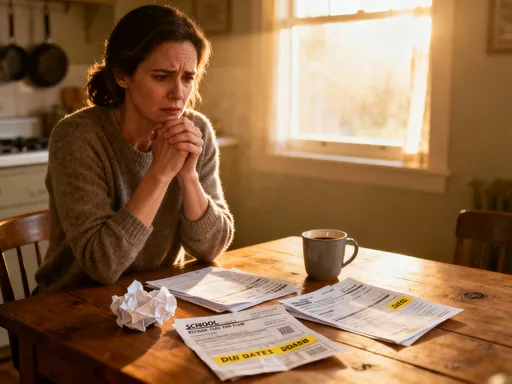

The Hidden Costs of "Normal" Spending

Some expenses appear harmless because they’re common, socially accepted, or feel small in isolation. But frequency and compounding turn these choices into major financial drains. The real cost of a daily $5 coffee isn’t just $5—it’s $150 a month, $1,800 a year, and over $50,000 in lost investment growth over 30 years, assuming a modest 7% annual return. That’s not hyperbole. It’s math. The same principle applies to financing electronics, eating out multiple times a week, or using credit cards without a repayment plan. Each decision carries not just a price tag but an opportunity cost—the value of what you could have done with that money instead.

Take the example of buying a smartphone on a 24-month installment plan with interest. The advertised price might be $800, but with financing charges, the total cost climbs to $950. That extra $150 isn’t just an expense—it’s a tax on convenience. Worse, it sets a precedent. When every purchase is financed, debt becomes routine, and financial agility disappears. Similarly, dining out five times a week at an average of $20 per meal adds up to $400 a month—$4,800 a year. That’s enough to cover a family vacation, a major home repair, or a significant boost to an emergency fund. Yet, because the spending happens in small increments, it rarely triggers alarm.

The deeper cost isn’t just monetary. It’s the erosion of choice. Every dollar spent on temporary convenience is a dollar not available for long-term goals. This isn’t about banning coffee or eating out. It’s about recognizing that normal doesn’t mean optimal. Many people operate on autopilot, assuming their spending habits are inevitable. But habits can be redesigned. A simple change—like preparing coffee at home four days a week—can save over $1,000 a year with minimal impact on lifestyle. The key is awareness. Once you see the long-term impact of small, repeated choices, you gain leverage. You’re no longer passive. You’re empowered to redirect those funds toward something more meaningful—whether that’s debt reduction, saving for a goal, or simply building confidence in your financial decisions.

Building a Lean Framework: Prioritizing Value Over Volume

Financial freedom isn’t built through deprivation. It’s built through discernment—choosing what truly adds value and letting go of what doesn’t. This requires a shift from cost-cutting as punishment to cost-optimizing as strategy. The goal isn’t to live with less. It’s to live better with intention. A lean financial framework isn’t about slashing every expense. It’s about aligning spending with what matters most. For one family, that meant cutting cable but investing in a high-speed internet plan to support remote learning and work. For another, it meant switching to generic groceries while maintaining a weekly date night. These aren’t sacrifices. They’re trade-offs—conscious decisions to fund priorities by reducing non-essentials.

One of the most effective strategies is focusing on quality over quantity. Buying durable, well-made items—even at a higher upfront cost—often saves money over time. A $120 pair of waterproof boots that lasts seven winters is cheaper than three $50 pairs that wear out in two years. The same logic applies to appliances, furniture, or even children’s clothing. Investing in longevity reduces replacement frequency and waste. Another powerful lever is timing. Waiting for sales, using cashback offers, or bundling services can yield significant savings without changing lifestyle. For instance, combining internet and phone service through one provider might save $30 a month—$360 a year—compared to separate plans.

Meal planning is another high-impact habit. One study found that households that plan meals save an average of $1,500 annually while reducing food waste. The process doesn’t require gourmet skills. It starts with a weekly menu, a shopping list, and a commitment to stick to it. This simple routine eliminates impulse buys, reduces trips to the store, and cuts down on takeout. Over time, it becomes automatic. The savings aren’t just financial. They extend to time and stress—fewer decisions during busy weeks, less guilt about waste, and more control over nutrition. Building a lean framework isn’t about perfection. It’s about progress—making one or two sustainable changes that compound into lasting results.

Risk Control: Protecting Gains Without Overcomplicating

Accumulating savings is only half the battle. Protecting them is equally important. Many people focus on growth—earning interest, investing, or finding deals—but overlook the role of risk control. True financial security comes not just from what you gain, but from what you preserve. The most effective risk management strategies are often the simplest. An emergency fund, for example, isn’t glamorous, but it’s transformative. Having three to six months’ worth of essential expenses saved in a liquid, accessible account provides a buffer against surprises. Whether it’s a car repair, a medical bill, or a temporary job loss, that cushion prevents small setbacks from becoming financial crises.

Insurance is another critical layer of protection. Health, home, auto, and disability insurance aren’t expenses—they’re safeguards. They transfer risk from you to an institution better equipped to handle it. Skipping coverage to save money is a false economy. A single uninsured accident or illness can wipe out years of savings. The key is balance—carrying adequate coverage without overpaying. Shopping around every few years, bundling policies, or adjusting deductibles can reduce premiums without sacrificing protection. Life insurance, particularly for parents or dependents, ensures that loved ones aren’t burdened by debt or loss of income if something happens.

Equally important is avoiding over-leveraging. Debt isn’t inherently bad—mortgages and student loans can be tools for building long-term value. But when debt grows faster than income, or when it’s used for depreciating assets like cars or vacations, it becomes a drag. High-interest credit card debt is especially dangerous, with rates often exceeding 20%. Paying only the minimum can extend repayment for decades and double the original cost. The goal isn’t to eliminate all debt, but to manage it wisely—prioritizing high-interest balances, avoiding unnecessary borrowing, and never relying on credit to fund lifestyle. Risk control isn’t about fear. It’s about freedom—the freedom to make choices without panic, to weather storms without derailing progress, and to sleep soundly knowing you’re prepared.

Turning Savings Into Momentum: The Quiet Power of Reinvestment

Saving money is a victory. But the real transformation happens when those savings are put to work. Idle cash loses value over time due to inflation. But redirected funds—once spent on leaks or low-value habits—can generate long-term gains. This is the power of reinvestment. Every dollar saved becomes a seed for future growth. The most effective strategy is to automate this process. Set up automatic transfers to savings, retirement accounts, or debt payments as soon as income arrives. This ensures that progress happens consistently, without relying on willpower or perfect timing.

One of the highest-impact uses of saved funds is accelerating debt repayment. Applying extra payments to high-interest debt reduces both the principal and the total interest paid. For example, adding just $100 a month to a credit card payment can shave years off the repayment timeline and save thousands in interest. That same $100 directed toward a student loan or car loan creates similar benefits. Once high-interest debt is under control, the focus can shift to building wealth. Increasing contributions to a 401(k) or IRA—even by small amounts—takes advantage of compound growth. Over decades, even modest contributions can grow into substantial retirement funds.

Reinvestment also includes funding personal growth. Using saved money for a certification, a workshop, or a skill-building course can increase earning potential over time. A $500 investment in a professional development program might lead to a promotion or side income that pays for itself many times over. Similarly, allocating funds toward home improvements that increase efficiency—like insulation, energy-efficient windows, or solar panels—can reduce long-term utility costs. These are not expenses. They are investments in comfort, sustainability, and value. The psychological effect of reinvestment is just as important as the financial one. Watching progress—seeing debt shrink, savings grow, or skills expand—creates motivation. It turns discipline into a reward system. You’re no longer just cutting back. You’re building something.

Freedom by Design: Living Lighter, Not Poorer

Financial freedom isn’t a number in a bank account. It’s a state of mind—a sense of control, choice, and calm. It means waking up without dread about bills, having the flexibility to say no to unfulfilling work, and being able to handle life’s surprises without panic. This kind of freedom doesn’t come from extreme frugality or sudden windfalls. It comes from consistent, thoughtful choices about money. It’s built not on what you earn, but on how you manage, protect, and grow what you have. And it’s accessible to anyone willing to pay attention.

When you align spending with values, money becomes a tool rather than a source of stress. You might choose to downsize your home to spend more time with family. You might leave a high-paying job for one that offers better balance. You might fund a dream of travel, volunteering, or starting a small business. These choices aren’t possible because of a big salary. They’re possible because expenses are under control, savings are growing, and risk is managed. The lightness comes not from having less, but from carrying less emotional weight. You’re no longer chasing the next paycheck to cover the last purchase. You’re living with intention.

This journey doesn’t require perfection. It requires awareness, patience, and a willingness to start. Track your spending. Identify leaks. Make one change. Build a buffer. Redirect one stream of cash. Over time, these steps compound. The goal isn’t to live poorly. It’s to live fully—with less noise, less pressure, and more room for what truly matters. Financial freedom isn’t about having everything. It’s about needing less and choosing more. And that, more than any dollar amount, is the quiet foundation of a life well lived.