Why Cultural Inheritance Could Break Your Family’s Future — And How Diversification Saves It

I used to think passing down family wealth was about wills and signatures. Then I watched a cousin’s inheritance spiral into conflict — all because everything was tied to one asset. Cultural inheritance isn’t just heirlooms and traditions; it’s emotional weight, expectations, and blind spots. I’ve seen estates shattered not by greed, but by poor planning. The real danger? Putting all your legacy in one basket. Let me show you how to protect what matters — before it’s too late.

The Hidden Cost of Sentimental Wealth

Family wealth often carries deep emotional meaning, especially when tied to cultural identity. An ancestral home, a piece of farmland, or a small business passed through generations can symbolize continuity, pride, and belonging. For many families, these assets are more than investments — they are living testaments to survival, hard work, and heritage. But when financial decisions are made primarily out of sentiment, the consequences can be quietly devastating. Emotional attachment can cloud judgment, leading families to preserve assets long after they cease to serve a practical or profitable purpose. This emotional anchoring often prevents necessary financial evolution, turning what was once a source of stability into a growing liability.

Consider the case of a rural family farm inherited by three siblings. Two live in cities and have stable careers, while one stayed behind to manage the land. Over time, crop prices decline, maintenance costs rise, and government subsidies shrink. Yet, the idea of selling — or even leasing — the farm is met with resistance. "It’s been in our family for 100 years," one sibling says. "Selling would feel like betrayal." The result? The sibling who lives on the land bears all the burden, while the others benefit emotionally but contribute nothing. The farm loses value, taxes go unpaid, and resentment builds. No legal dispute has occurred — yet the family is already fractured. This is not an isolated story. Across cultures and continents, families cling to assets not because they are valuable, but because they feel irreplaceable.

The financial paralysis caused by sentimental wealth often manifests in delayed decision-making. Families may avoid appraisals, skip estate planning, or refuse to consider partial liquidation, fearing that any change will erode tradition. But inaction is not neutrality — it is a choice with compound consequences. As inflation rises and markets shift, a single-asset estate becomes increasingly vulnerable. Without diversification, families expose themselves to concentrated risk: if the asset fails, everything fails. Moreover, younger generations may feel trapped, unable to pursue education, relocation, or entrepreneurship because their inheritance is locked in an illiquid form. The very thing meant to empower them instead restricts their freedom. Sentiment, when unchecked, becomes a silent tax on future opportunity.

When Inheritance Turns Into Conflict

Inheritance disputes rarely begin with shouting matches or court filings. They start quietly — with assumptions, unspoken expectations, and unequal burdens. When a family’s wealth is concentrated in one asset, such as a home or business, the potential for conflict multiplies. Siblings may agree in principle that the asset should stay in the family, but disagree sharply on how it should be used, maintained, or shared. One may want to sell and divide the proceeds, another may wish to live in the home, and a third may advocate for renting it out. Without clear agreements, these differences can escalate into lasting rifts. What begins as a disagreement over floor plans or rental income can end in severed relationships, years later.

One common trigger is perceived fairness. In many families, the belief persists that inheritance must be divided equally. But equality does not always mean fairness. Imagine two siblings: one has supported aging parents for years, managing medical appointments and household repairs, while the other lives abroad and visits only occasionally. When the parents pass, both inherit the home equally. The sibling who stayed feels this is unjust — they contributed more, emotionally and financially, yet receive the same legal share. Resentment grows, especially if the absent sibling insists on selling the property they never maintained. This imbalance is not about greed; it’s about recognition. When assets are undiversified, there are fewer ways to acknowledge differing levels of contribution, leading to feelings of invisibility and betrayal.

Another source of tension is unclear roles. Who is responsible for upkeep? Who decides when repairs are needed? Who collects rent, if any? Without formal structures like trusts or family agreements, these decisions fall to whoever is most involved — often the most available, not the most qualified. This can create power imbalances, where one sibling becomes the de facto manager, making unilateral choices that others later challenge. Over time, this erodes trust. Disputes may be avoided for years, but they rarely disappear. They simmer beneath the surface, resurfacing during moments of stress — a medical emergency, a job loss, or a divorce — when access to cash becomes urgent. By then, communication has broken down, and cooperation feels impossible. The asset, once a symbol of unity, becomes a battleground.

The Myth of the Family Legacy Asset

Many families believe that their legacy hinges on preserving a single, central asset — a farmhouse, a shop, a seaside cottage. This belief is powerful, often passed down with stories of ancestors who built something from nothing. There is dignity in that history, and preserving it can feel like honoring those who came before. But the assumption that legacy equals physical preservation is a myth — and a dangerous one. A farm that once supported five families may now generate barely enough to cover taxes. A downtown storefront may be overshadowed by online competition. A house in a declining neighborhood may lose value year after year. Yet, families continue to pour money into these assets, not because they are sound investments, but because they are symbols.

The problem is not the symbol itself, but the refusal to adapt. Legacy should not be defined by what is kept, but by what is enabled. True legacy is not measured in square footage or property deeds, but in opportunity, security, and resilience. When families insist on preserving a single asset at all costs, they often sacrifice the very things that would honor their ancestors: upward mobility, education, and financial independence for the next generation. A great-grandparent who worked the land would likely want their descendants to have choices, not be bound to a failing plot of soil. Yet, cultural pride can make it difficult to admit that the old model no longer works.

Over-reliance on one asset also creates financial fragility. If 90% of a family’s net worth is tied to a single property, a market downturn, natural disaster, or regulatory change could wipe out decades of wealth in months. Unlike diversified portfolios, which can absorb shocks in one sector, undiversified estates have no buffer. When the family business fails, there is no stock portfolio to fall back on. When the house needs $50,000 in repairs, there is no liquid fund to cover it — only debt or forced sale. The irony is that the very thing meant to secure the future becomes its greatest risk. Legacy, in this case, is not being preserved — it is being gambled.

Diversification as Cultural Protection

Diversification is often misunderstood as abandonment. To some, selling a family home or closing a generational business feels like surrendering identity. But the opposite is true. Diversification is not betrayal — it is responsibility. It is the act of ensuring that cultural values survive not through rigid preservation, but through active stewardship. By converting concentrated wealth into a range of assets, families gain flexibility, reduce risk, and create opportunities for every member. This is not about erasing tradition; it is about evolving it so it can endure.

Consider a family that decides to sell an aging commercial property. Instead of dividing the cash equally and ending the conversation, they use the proceeds to build a shared future. One portion funds college accounts for grandchildren. Another is placed in a low-volatility investment portfolio, generating steady income for family reunions, cultural events, or elder care. A third supports a community initiative — a scholarship for local students, a heritage festival, or a small grant program for young entrepreneurs within the family. In this model, the physical asset is gone, but its value lives on in ways that actively support the family’s values. The legacy is not lost — it is multiplied.

Diversification also relieves pressure on individual members. When wealth is spread across liquid and income-generating assets, no one person has to shoulder the full burden of upkeep or decision-making. A sibling who wants to pursue a career in art or education isn’t forced to return home to manage a farm. A niece who dreams of studying abroad isn’t held back because the family’s wealth is locked in real estate. Each member can pursue their path, knowing they have access to resources that were prudently managed. This is not cold finance — it is care in action. It says, "We value you not for what you maintain, but for who you are."

Practical Steps to Balance Culture and Finance

Starting the conversation about diversification does not require a lawyer or a financial advisor — it begins with a meal, a gathering, a moment of honesty. The goal is not to announce a sale, but to understand what the asset truly means to each person. Is it a home? A duty? A dream? A burden? These emotional truths must be acknowledged before any financial plan can succeed. Families that rush into legal restructuring without addressing these feelings often face resistance, silence, or passive sabotage. The process must be inclusive, patient, and respectful of generational differences.

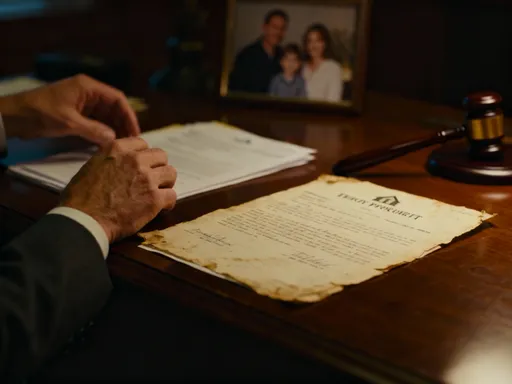

One effective approach is the phased transition. Instead of selling an ancestral home outright, a family might first lease it to trusted tenants, generating income while maintaining ownership. The rental revenue can fund family needs or be reinvested. Over time, as elders pass and younger members settle into their lives, the family can reassess. Another option is shared ownership through a limited liability company (LLC) or trust, which clarifies responsibilities, defines voting rights, and establishes a governance structure. This prevents one person from making unilateral decisions while ensuring the asset is managed professionally.

Another practical step is valuation. Many families operate under assumptions about an asset’s worth without ever obtaining a professional appraisal. A house believed to be worth $800,000 may, in reality, require $200,000 in repairs and sit in a declining market. Knowing the true financial picture allows for informed choices. It also helps dispel myths — such as the belief that "this land will only go up in value." Armed with facts, families can discuss options without fear or fantasy. Education is equally important. Hosting a session with a neutral financial planner can help members understand concepts like liquidity, tax implications, and risk exposure in simple terms. Knowledge reduces anxiety and builds consensus.

Risk Control: Avoiding the Downfall Traps

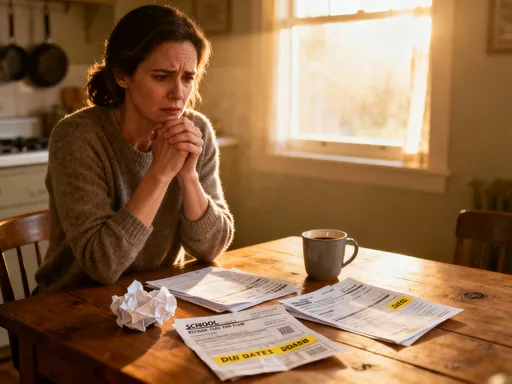

Undiversified estates are vulnerable to a range of predictable yet preventable risks. Market volatility is one of the most obvious. Real estate values fluctuate; business revenues decline; farmland can be damaged by drought or flooding. When a family’s wealth is concentrated in one of these areas, a single adverse event can trigger a chain reaction. A drop in property value may make refinancing impossible. A failed crop can lead to debt. Without alternative assets, families have no way to absorb these shocks. Liquidity crises are especially dangerous. When unexpected expenses arise — a medical emergency, a legal issue, or urgent repairs — families may be forced to sell at the worst possible time, often at a loss.

Succession gaps are another common trap. Many family businesses or properties lack a clear successor. The current generation assumes a child will take over, but that child may have no interest, training, or capacity. When the elder passes, the asset falls into disrepair or is mismanaged by default. Without a succession plan, even willing heirs may struggle to step in, especially if they lack financial literacy or business experience. This is not failure of character — it is failure of preparation. Diversification helps by reducing dependence on any one person to carry the entire burden. Instead of relying on a single heir, a diversified estate can support multiple paths, ensuring that no individual is overwhelmed.

Tax obligations are another silent threat. In many countries, inheritance or estate taxes must be paid in cash, even if the estate consists mostly of illiquid assets. Families that cannot liquidate part of the property may be forced to sell under duress or take on high-interest loans. Spreading assets across liquid investments ensures that cash is available when needed, preserving the core holdings. Additionally, diversified portfolios can be structured to minimize tax liability through strategies like step-up in basis, gifting, or trust allocations. These are not loopholes — they are tools available to any family willing to plan ahead. Risk control is not about pessimism; it is about prudence. It is the difference between reacting in crisis and acting with foresight.

Building a Legacy That Lasts Beyond One Generation

True wealth is not what you own — it is what you enable. A legacy that lasts is not measured in deeds or titles, but in freedom, education, and opportunity. When families diversify their assets, they are not abandoning tradition — they are strengthening it. They are ensuring that cultural values like resilience, care, and perseverance are passed down not as burdens, but as gifts. A granddaughter who receives a college fund rooted in the sale of a family shop is not disconnected from her heritage — she is empowered by it. A grandson who inherits a share of a balanced portfolio is not less honored — he is better equipped to build his own future.

The goal is not to erase the past, but to honor it by allowing it to evolve. Traditions that survive are not frozen; they adapt. A family that once measured success by land ownership may now measure it by graduation rates, business launches, or community contributions. These are not lesser achievements — they are modern expressions of the same values. Diversification allows families to honor their roots while planting new ones. It shifts the focus from preservation to progress, from obligation to possibility.

Ultimately, the most powerful legacy is choice. When heirs inherit not just a single asset, but a range of opportunities, they are free to define success on their own terms. They can honor their ancestors not by repeating the past, but by building a future that reflects both respect and innovation. This is the real act of love — not holding on, but letting go with wisdom. By spreading wealth wisely, families protect not only their finances, but their unity. They ensure that the next generation inherits not a burden, but a foundation. And in doing so, they create a legacy that doesn’t merely survive — it thrives.